In a crisis, people always come first.

Businesses are built and run by people. As a C-level leader, losing the trust and confidence of your people during a crisis can worsen the situation significantly.

How you treat people in a crisis will be remembered—long after the crisis has passed.

From leading multiple organizations through financial and operational crises, here’s what I’ve learned:

- Be transparent and timely in your communication—good news or bad.

- If you don’t yet have a clear plan, say so. But also share what you do know, and what people can focus on while the plan is being developed.

- Deliver bad news with a credible plan for what’s next and what you need from your team.

- Hone your message and communicate it clearly, consistently, and constantly.

- Be visible, available, and open to input. That doesn’t always mean in person—video calls, phone, or even a thoughtful email count. Respect and openness build trust.

Also: you can’t lead others if you can’t lead yourself. There are plenty of resources out there—especially during Covid-19—that focus on managing your own physical and mental health in a crisis. Use them.

And Then: Focus on Cash

The future of your business starts with cash.

- Do you know how much cash is available in the bank right now?

- Can you make your next payroll? What about the one after that?

- Do you have a credit line or other source of temporary funding?

- If you use it, how will you pay it back?

Too many business owners—especially in high-growth or stable times—don’t have clear answers to these basic questions. That’s a major risk.

If you’re confident in your cash picture, great. If not—or if you know someone who isn’t—please read on and share.

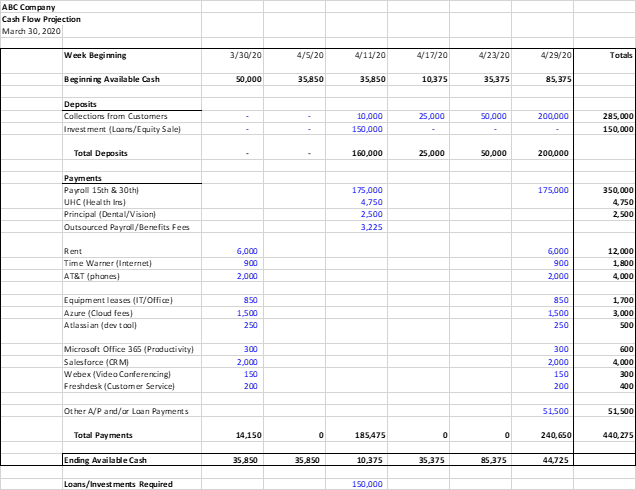

Here’s a simple weekly cash flow forecast you (or your finance lead) can build in a spreadsheet:

Cash in the bank today

+ Cash coming in (receivables, funding)

– Cash going out (payroll, rent, other expenses)

= Cash at end of week

That’s it. Round numbers are fine. Don’t overthink it.

Here is an example spreadsheet:

In the above example:

- The company is a SaaS business, but the model can be customized to fit any industry.

- They pay bills monthly, which simplifies cash management.

- A shortfall in the second week triggers a $150,000 line-of-credit draw—then repayments begin by month-end.

Run the numbers for at least a month, and create versions for different scenarios. If you can’t make payroll—or pay it back—you’ve got a problem. Better to see it now than too late. Short term cash planning should go out at least 12 weeks.

What If There’s a Shortfall?

Some short-term moves:

- Accelerate collections—especially from large customers (carefully)

- Delay non-critical vendor payments

- Delay payroll with transparency and a recovery plan

- Temporary layoffs or furloughs—with clarity and respect

- Permanent reductions—as a last resort

You may have other options. But the point is: you can’t act if you don’t know.

This blog’s goal is simple: help leaders become more proactive in managing through crisis.

If you remember nothing else, remember this:

Start with people. Know your cash. Lead with clarity.

Up next: Adapting Your Business for Post-Crisis Success.